Visa VAMP 2025: The New Rules Reshaping High‑Risk Payment Processing

Visa’s VAMP program is not just a policy tweak, it’s a paradigm shift. By holding acquirers accountable for the collective risk of their portfolios, Visa forces every merchant to take fraud and dispute management seriously. Industries with surging chargebacks, ecommerce, travel & hospitality, CBD/nutraceuticals, subscriptions, gaming, telemedicine, and high‑risk financial services, must adapt or risk losing access to payment processing.

No hidden fees. Ever.

Real-time accounting

SOC 1 & SOC 2 compliance

Expert human support

Table of Contents

Visa’s New Thresholds for Fraud and Disputes

Visa’s Acquirer Monitoring Program (VAMP), launching in mid‑2025, consolidates the card network’s fraud and dispute monitoring frameworks into a single VAMP Ratio. Under VAMP, both fraud alerts (TC40) and chargebacks (TC15) are counted against every merchant’s total transaction volume. Acquirers face an “above standard” tier at roughly 0.50 % of processed transactions and an “excessive” tier near 0.70%. Merchants themselves initially fall under a 2.2 % combined fraud‑plus‑chargeback threshold, which will tighten to roughly 1.5 % or less in 2026. Going forward, acquirers are obliged to police their portfolios aggressively; merchants with elevated dispute ratios risk fines, higher fees, rolling reserves, or even account termination. In this report we examine how VAMP affects industries where disputes have been surging.

Industry Impacts of VAMP

Ecommerce: Surging Disputes and Friendly Fraud

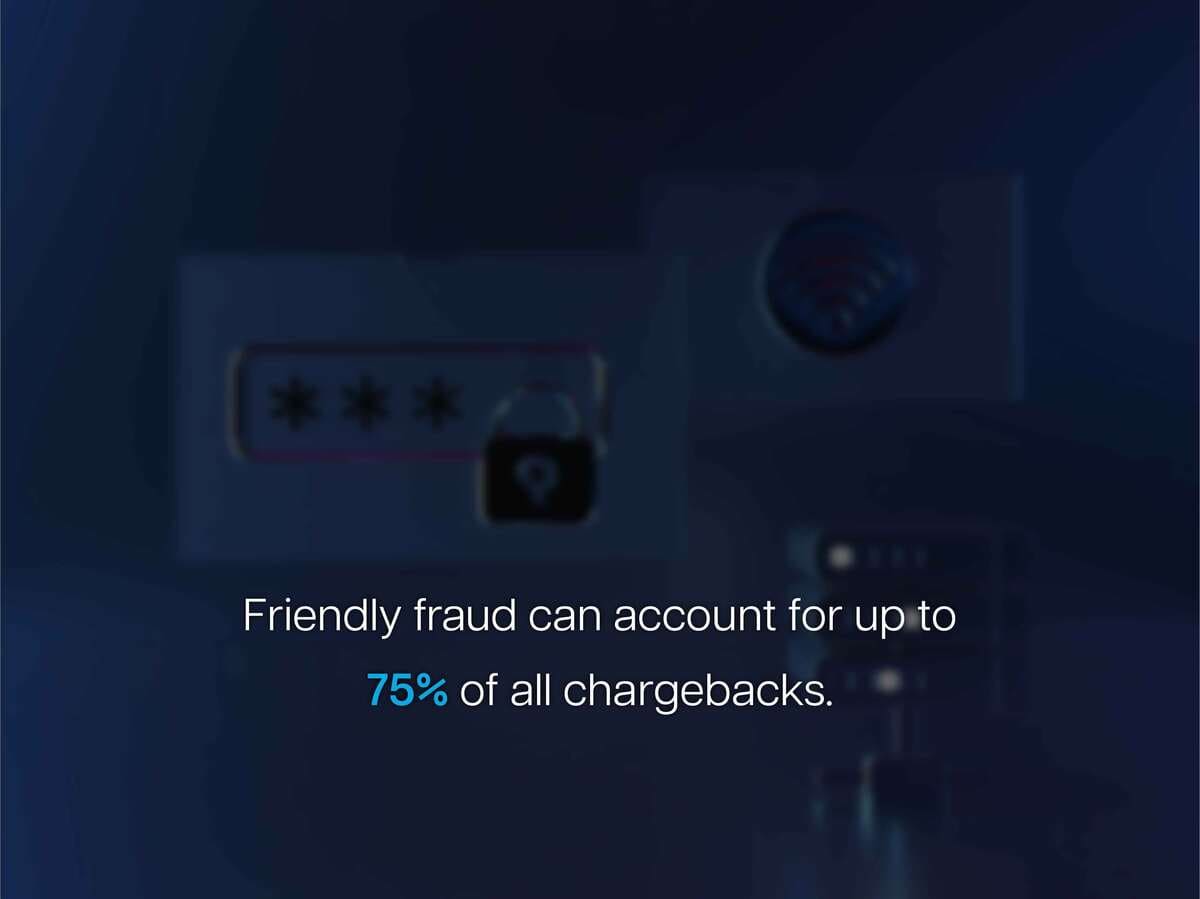

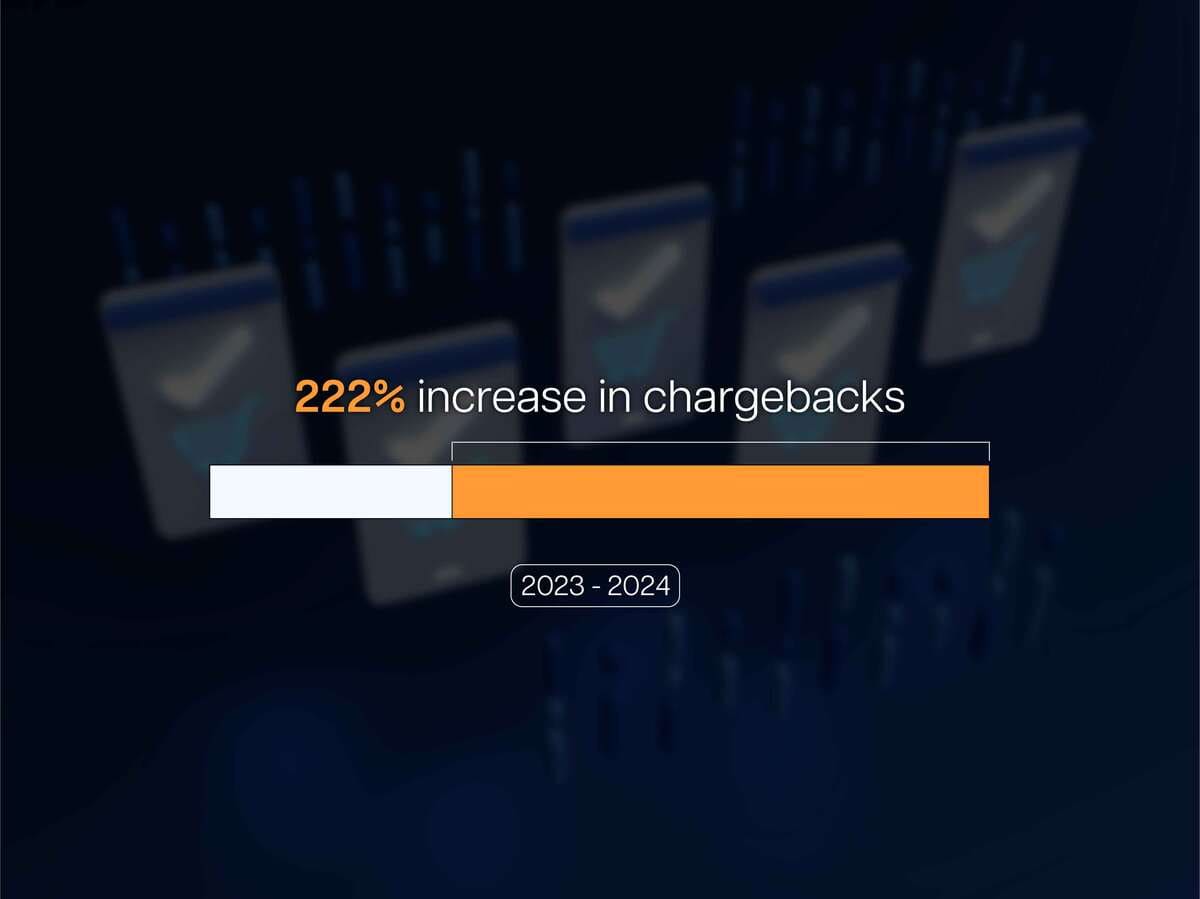

Dispute volumes are exploding across online retail. Sift’s 2024 chargeback data revealed that e‑commerce saw a 222% increase in chargebacks between Q1 2023 and Q1 2024 (1). Much of this growth comes from so‑called “friendly fraud” – consumers filing chargebacks on legitimate purchases. According to Chargebacks911’s 2024 field report, 72% of merchants surveyed reported an increase in chargebacks over the past three years, with an average spike of 18% (2). The problem isn’t isolated to disputed shipments either – subscription billing drives confusion and disputes. A 2024 Sift analysis found that 22% of consumers filed chargebacks specifically to cancel unwanted subscriptions and that 70% of consumers had filed at least one dispute in the prior year, with 22% filing two disputes (3). Visa’s own data suggests friendly fraud can account for up to 75% of all chargebacks, while Mastercard estimates 70% of all credit‑card fraud involves misuse of the chargeback process (4).

The takeaway for ecommerce merchants is clear: recurring billing models and unclear descriptors invite disputes. Under VAMP, even a modest uptick in these disputes could jeopardize an acquirer’s portfolio, prompting stricter underwriting, reserves, or off‑boarding. Merchants must embrace 3‑D Secure authentication, improve billing clarity, send pre‑renewal reminders, and implement dispute‑alert services to intercept refunds before they become chargebacks.

Travel & Hospitality: High‑Ticket Sector at Risk

No sector has seen a sharper rise in disputes than travel and hospitality. A 2024 Sift‑derived report cited by The Paypers found that online travel and lodging businesses experienced an astonishing 816% increase in chargebacks (1). E‑commerce experienced a 222% rise and digital goods a 59% uptick in the same period, but travel dwarfs them all. The industry’s financial exposure is enormous: Chargeback Gurus’ 2024 travel report estimated that the travel and hospitality sector faced roughly $25 billion in chargebacks in 2023 (5). Losses are not limited to reversal fees. Sertifi’s hospitality fraud analysis notes that roughly 5–6% of the industry’s $3 trillion in revenue, around $150 billion, is lost to fraud (6).

What drives these losses? Cancellation confusion is a key factor. The State of Chargebacks in the Travel & Hospitality Industries report found that over 30% of chargebacks come from unclear cancellation policies (5). Friendly fraud is also rampant: nearly 40% of disputes in travel are fraudulent (5). On the consumer side, Sertifi notes that around half of all hotel guests dispute transactions instead of requesting refunds (6). To make matters worse, Payrails reports that hospitality businesses have endured a 30%+ year‑over‑year rise in chargebacks for several years (6). Those trends, combined with larger transaction sizes and seasonal spikes, mean travel merchants are often the first to push acquirers into VAMP’s danger zone.

Survival strategies include clear, accessible cancellation and refund policies; automatic refund offers for weather or pandemic‑related cancellations; 3‑D Secure authentication for high‑value bookings; and participation in Visa’s Rapid Dispute Resolution program. By intercepting disputes early, travel businesses can reduce their VAMP ratio and keep their acquirer relationships intact.

CBD, Nutraceuticals & Telemedicine: High‑Risk by Definition

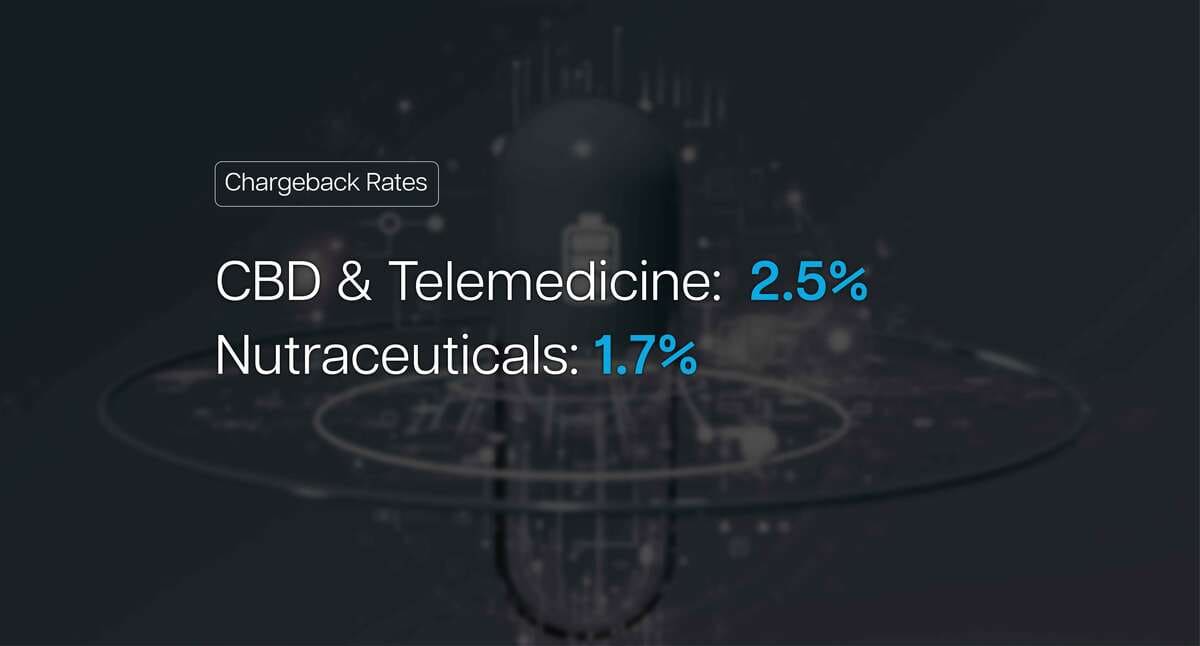

Certain verticals attract regulatory scrutiny and elevated dispute rates by their very nature. A 2025 Seamless Chex industry table notes that CBD merchants see an average 2.5% chargeback rate, while nutraceutical sellers average 1.7% (7). Telemedicine merchants see 2.5% chargeback rates as well (7). These figures far exceed Visa’s VAMP targets, putting such businesses squarely in the high‑risk bucket. The subjective nature of health and wellness products contributes to refund requests (“it didn’t work”), and the recurring billing models common in supplements increase the likelihood of dispute.

Telemedicine faces additional legal risk. In July 2025 the U.S. Department of Justice announced that forty‑nine defendants submitted $1.17 billion in fraudulent Medicare claims involving telemedicine and genetic testing (8). Such high‑profile cases can sour consumer trust and drive legitimate patients to dispute charges when insurance denies coverage. For CBD and nutraceutical merchants, inconsistent regulations (hemp legality varies by jurisdiction) add further uncertainty. Under VAMP, these merchants must carefully manage chargebacks, document customer authorization, and provide transparent product information to avoid being shut off by conservative acquirers.

Subscription & Digital Services: Recurring Disputes and Consumer Confusion

Subscriptions are essential for SaaS providers, online education platforms, coaching services, and content creators. However, they also generate steady streams of disputes. Chargeflow’s 2024 industry study found that digital goods and subscription services saw a 59% increase in chargeback rates from 2023 to 2024 (1). Sift’s research shows that 22% of consumers file chargebacks specifically to exit subscriptions, and that 70% of customers filed at least one dispute in the last 12 months, with 22% filing two disputes (3). These numbers illustrate how misunderstanding of auto‑renewals and poor cancellation processes fuel a disproportionate share of VAMP‑counted disputes.

Merchants offering subscriptions should provide multiple reminders before renewal, one‑click cancellation, and clear billing descriptors. Using Visa’s Order Insight or similar tools to provide itemized purchase details at the time of dispute can also reduce cases where customers claim to not recognize the charge.

Online Gaming & Gambling: Fraud and Bonus Abuse

The digital gaming and gambling industry faces a perfect storm: high transaction volumes, anonymous users, and constant fraud attempts. Sumsub’s 2024 iGaming Fraud Report documented that fraud in online casinos and betting platforms increased 64% year‑over‑year between 2022 and 2024 (9). The same report notes that fraud losses for mobile casinos and betting platforms totaled $1.2 billion between 2022 and 2023 (9). These numbers reflect not only stolen‑card attacks but also bonus abuse (multiple accounts claiming promotions) and “friendly fraud” (players disputing losses).

Financial Services: Credit Repair & Debt Relief

Financial‑services merchants, credit repair companies, payday lenders, and debt consolidators are also high risk under VAMP. They often collect payment up front and deliver intangible services, making disputes common. In January 2025 the U.S. Federal Trade Commission announced that it returned over $3.5 million to consumers who were scammed by a credit‑repair operation known as “The Credit Game” (10). While this refund came from enforcement, it underscores how regulators and card networks view the sector.

What Merchants Should Do: Survival Strategies

VAMP shifts responsibility up the supply chain. Acquirers face fines if merchants in their portfolios generate too many disputes, so they will either pressure merchants to lower their ratios or sever relationships. To thrive under VAMP, merchants should:

- Aim well below the 1 % mark. Although Visa’s initial merchant threshold is 2.2 %, acquirers are incentivized to keep portfolios under 0.5 %. Maintaining a dispute ratio closer to 0.3–0.5 % provides a buffer.

- Adopt strong authentication. Implement 3‑D Secure (EMV 3DS) for all online transactions. Visa shifts liability for fraud to issuers when authentication is used, preventing many chargebacks from counting toward the VAMP ratio.

- Use dispute‑alert services. Services like Visa Rapid Dispute Resolution and Ethoca/Verifi alerts notify merchants when customers raise disputes, allowing them to issue refunds before the chargeback posts. Since pre‑dispute refunds don’t count toward VAMP, this can dramatically lower ratios.

- Clarify billing descriptors and policies. Use a recognizable merchant name on statements, send confirmation emails, and provide easy access to cancellation or refund options. Clear communication reduces “I don’t recognize this charge” disputes.

- Monitor metrics and segment risky transactions. Track dispute and fraud rates monthly by product line or marketing source to identify problematic areas. Consider routing high‑risk orders (e.g., high‑value, cross‑border) through specialist high‑risk accounts to protect your core merchant account.

- Partner with a high‑risk payment expert. Firms like Revitpay specialize in onboarding and managing merchants in challenging categories. They provide tools to monitor VAMP metrics, implement fraud screening, and manage chargeback responses, helping merchants stay off Visa’s watch lists.

At RevitPay, we're more than just a processor, we’re a risk partner. Since Visa first announced VAMP, we have worked closely with our merchants to break down what these new risk thresholds really mean for their business. By helping merchants understand how fraud and disputes affect their processing stability, we’ve empowered them to make smarter decisions, reduce chargeback ratios, and retain their ability to scale. Education is a powerful tool, and we’ve made it a core part of how we support merchants navigating high-risk industries. Our team has already helped high-risk merchants across various verticals implement tailored fraud mitigation strategies. Under VAMP, that kind of support isn’t optional. It’s survival.

Conclusion: Adapting to VAMP’s New Reality

Visa’s VAMP program is not just a policy tweak, it’s a paradigm shift. By holding acquirers accountable for the collective risk of their portfolios, Visa forces every merchant to take fraud and dispute management seriously. Industries with surging chargebacks, ecommerce, travel & hospitality, CBD/nutraceuticals, subscriptions, gaming, telemedicine, and high‑risk financial services, must adapt or risk losing access to payment processing. The statistics tell the story: triple‑digit growth in travel disputes, billions lost to fraud in iGaming, and millions refunded in credit‑repair scams. Under VAMP, even legitimate merchants with dispute ratios above 1 % may find their processor relationships in jeopardy.

Fortunately, the path forward is clear. Embracing strong customer authentication, transparent billing, proactive dispute resolution, and specialized high‑risk acquirers can keep merchants well below the new thresholds. With vigilance and the right partners, businesses can turn VAMP from a threat into an opportunity to modernize fraud prevention and build lasting customer trust.

References

[1] The Paypers – Chargeback Fraud Surges (2024)

[2] FF News – 72% of Merchants Report Increase in Chargebacks (2024)

[3] Sift – 2024 Chargeback Analysis

[4] DataVisor – Preventing Friendly Fraud (2024)

[5] Chargeback Gurus – Impact on Travel and Hospitality (2024)

[6] Sertifi – Hospitality Fraud Statistics (2024)

[7] Seamless Chex – Chargeback Rates by Industry (2025)

[8] Health Law Advisor – DOJ Healthcare Fraud Takedown (2025)

[9] Sumsub – iGaming Fraud Report (2024)

[10] U.S. Department of Justice – FTC Refund Announcement (2025)

Supercharge your Payments

RevitPay is here to help you scale smarter — from your 1st transaction to your 100,000th.

Previous

Next

Frequently Asked Questions

Recent Articles

A Seamless Start to Smarter Payment Processing

Request an Application

Submit for Approval

Start Processing

Explore More Online Payment Solutions

Everything you need to process payments wherever, whenever.

Seamless & Secure Payment Processing

Payment Methods That Power High Risk Businesses

We offer a wide range of secure, flexible payment methods tailored to the needs of high risk merchants. From credit card processing and mobile payments to ACH, eCheck, and more, our solutions are built to help your business accept payments confidently.

Credit Cards

Fast, familiar, and essential.

Give your customers the convenience of paying by credit card while maintaining the fraud protection and flexibility high risk merchants need.

Mobile Payments

Payments on the go.

Whether in-store or remote, accept transactions via smartphones and tablets, keeping your business agile and responsive.

Bitcoin & Crypto Payments

Stay ahead of the curve.

Expand your payment options to bypass traditional banking barriers and get paid faster—with global reach and fewer limitations.

MOTO Payments

Mail and telephone orders made easy.

Process card-not-present transactions securely with MOTO functionality, ideal for businesses that take payments by phone or through manual orders.

ACH Payments

Lower fees, higher reliability.

Automated Clearing House (ACH) payments are perfect for recurring billing or high-ticket items, offering a secure, bank-to-bank alternative to cards.

eCheck Payments

Modernize check payments.

Accept digital checks with ease, streamlining your processing while reducing risk and delays often associated with traditional paper checks.

Seamless Continuity Billing for Subscription-Based Businesses

Looking to support subscription models? Our Continuity Subscriptions solution offers automated recurring billing, built-in autobill features, and reduced payment churn—perfect for businesses that rely on predictable revenue.

Find the Right Way to Get Paid

Whether you’re running an online store, accepting payments remotely, or operating in a high risk space, RevitPay gives you the tools to process transactions with confidence and ease.

A Seamless Start to Smarter Payment Processing

Request an Application

Submit for Approval

Start Processing

Ready to get started?

Join businesses who are saving thousands each year with RevitPay.